Shared Ownership Overview

Shared Ownership is designed as a stepping stone to home ownership supporting first-time buyers get onto the property ladder.

It has been a popular buying scheme aimed to support those who otherwise wouldn't have been able to buy on the open market and comes with a number of benefits.

Also referred to as part buy part rent, Shared Ownership allows you to buy an initial share of 25% to 75% of the value of a home, and you’ll need to take out a mortgage to pay for your share of the home’s purchase price.

You will then pay a subsidised rent on the share you don’t own, and there will also be a service charge to make up the monthly cost of buying through Shared Ownership.

You can check out our Shared Ownership eligibility guide to see if you are eligible. It's important to weigh up the pros and cons of buying through Shared Ownership which is why we have put together a helpful guide to support you.

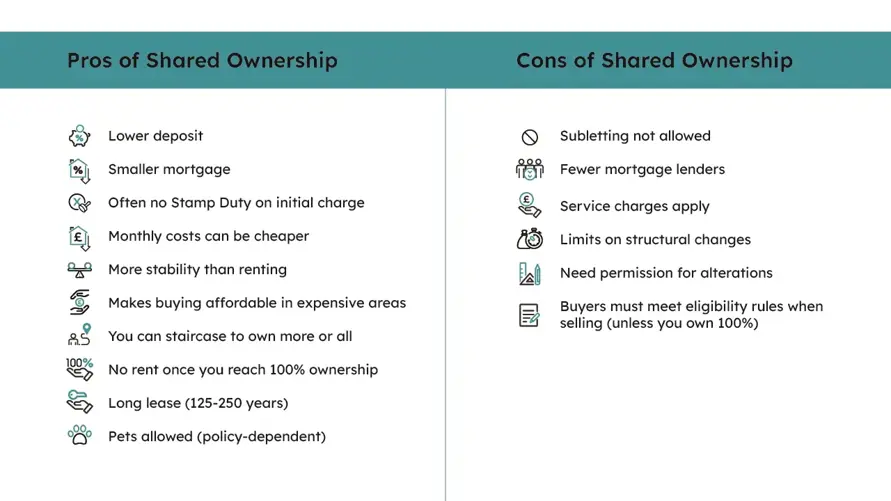

Pros of Shared Ownership

Buying a home through Shared Ownership comes with a number of fantastic benefits including:

✔ The deposit required on a Shared Ownership home is usually a lot lower than buying on the open market as you only need a deposit on the share rather than full market value of the home.

✔ As you require a smaller deposit and the overall value of the percentage bought is lower, obtaining a mortgage is likely to be more accessible even with a lower wage.

✔ As you only buy a percentage in the home, you are usually exempt from paying stamp duty if the share purchased is below the stamp duty threshold which is a big cost saving.

✔ With Shared Ownership, your monthly outgoings can often work out cheaper than if you bought a property on the open market and also renting privately in some instances.

✔ Buying through Shared Ownership will make you an 'owner-occupier' giving you much more stability and security for your living situation compared to renting.

✔ By buying only a share in the home makes home-ownership more affordable and means you can often buy a home in central London locations without compromise.

✔ You can buy more shares in your Shared Ownership home in the future which is a process known as 'Staircasing'. You can buy as much or as little as you want when you can afford to until eventually you own 100% of the home which will mean you own the home outright and pay no rent!

✔ As long as you keep up with rent and mortgage repayments on your home, you can live in the property for the duration of your lease usually 125 to 250 years.

✔ You have the option to sell your home at any time if you want to.

✔ You are free to have a pet in your Shared Ownership home as long as it meets the housing provider's pet policy.

Cons of Shared Ownership

✘ You can not sublet a Shared Ownership home.

✘ There are some mortgage lenders who don't offer Shared Ownership mortgages, meaning there are less available on the market, however, it is still available by the majority of major lenders.

✘ Shared Ownership properties are sold as a leasehold which is a long tenancy ownership where you will be given the right to occupy your home. The term of the lease will be fixed at the very beginning, decreasing in length each year, and the home can be bought or sold during that time.

✘ You will need to pay a service charge on your Shared Ownership home to cover the cost of communal spaces like most leaseholds.

✘ While you’re free to decorate internally, there are usually restrictions on what home improvements you can do. You will need to obtain permission from the relevant housing provider before you make any structural alterations to your home.

✘ When you come to sell your home, the buyer will also need to meet the eligibility criteria for Shared Ownership unless you have staircased to 100%.

Summary of Shared Ownership pros and cons

FAQs about the Pros and Cons of Shared Ownership

Selling a Shared Ownership home is known as a resale, and you can sell at any time. Peabody will help you market and find a buyer for your home. Peabody is an established provider of Shared Ownership homes so, we are well-placed to market and sell your home.

Shared Ownership allows first-time buyers to purchase a home with a smaller deposit, benefit from lower monthly costs, and gradually increase ownership through Staircasing. It offers more security than renting and can be a more affordable way to live in desirable areas, like London.

In many cases, yes. Shared Ownership can offer lower monthly costs compared to private renting, especially when factoring in the limits set on rent (a maximum of 2.75% of the unowned share) and the ability to build equity in your home over time.

No. Shared Ownership is available for both New Build and resale properties, meaning you can buy a previously owned Shared Ownership home if it better suits your budget or needs.

Homeowner Stories

Discover a collection of homeowner stories from previous Peabody New Homes purchasers and find out how we were able to help them onto the property ladder and find their dream home through Shared Ownership.

"We didn’t know how we would ever be able to get on the property ladder with a smaller deposit – then my Mum mentioned Shared Ownership!"

"Renting in Oxford is so expensive, we wanted to stay here long-term, but we wanted to make sure we invested in something for ourselves"

"A friend used Shared Ownership and recommended it. We love the fact we are paying something off for ourselves. "