Why do people turn to the Bank of Mum and Dad?

Parents step in to help their children for a variety of reasons: to fund their deposit, improve mortgage affordability, reduce the need for high-interest loans, or simply give their children a better chance at getting on the property ladder sooner.

It's become a very common practice in the UK since the 2008 crash, with 52% of first-time buyers having help from their parents in 2024 .

How can I help my child buy a home?

There are many different ways that parents can financially help their child buy a home. Some parents choose to gift money for a deposit, while others offer an informal or formal loan.

Support can also come in the form of acting as a guarantor on a mortgage or buying together through joint ownership. The best choice depends on both the parents’ financial situation and the child’s borrowing needs.

Can I gift my child money to buy a home?

Gifting money is one of the most common routes. Most lenders will accept a gifted deposit from parents, though they will usually require a letter confirming that the money is a genuine gift and not a loan.

Under gifted deposit rules in the UK, parents must declare they do not expect repayment, and proof of funds may be needed. While gifts from parents are normally acceptable, those from extended family can attract extra checks by lenders.

Are there any tax considerations?

Yes - and this is where families need to be cautious. There is no immediate tax to pay when gifting money, but inheritance tax rules may apply.

Parents can give up to £3,000 each year without it being added to their estate for IHT purposes. Larger gifts can still be tax-free if the parent lives for seven years after making them.

If they pass away within that period, the gift could be taxed depending on its value and timing. Seeking legal or financial advice is strongly recommended before gifting substantial amounts.

Should I talk to a financial advisor?

Given the financial and legal implications, speaking to a Financial Advisor or Mortgage Broker is often a wise move.

They can explain the risks of gifting versus lending, recommend the most suitable mortgage products, and help families understand how parental support might affect tax or inheritance planning.

Giving a loan to help your child buy a house

Not every parent is comfortable with giving money outright. Some prefer to lend funds instead. While this can work, it must be handled carefully. Lenders usually want to know if any part of the deposit is borrowed, and repayment terms should be agreed in writing.

A solicitor can draft a formal loan agreement to protect both sides and avoid future disputes.

The Pros and Cons of buying a home with help from your parents

Pros:

- A larger deposit provides access to better mortgage rates.

- Reduced borrowing costs make homeownership more affordable.

- Ability to buy a home sooner.

- Greater financial security and peace of mind for children.

Cons:

- Potential for family disagreements if expectations are unclear.

- Parents acting as guarantors or co-owners risk their own finances.

- Inheritance planning becomes more complex when large gifts or loans are involved.

How to buy a house with the Bank of Mum and Dad

Every family’s circumstances are different, so the right solution depends on what the parents can afford. Having an open discussion early on is key, and professional advice can help turn good intentions into a workable plan.

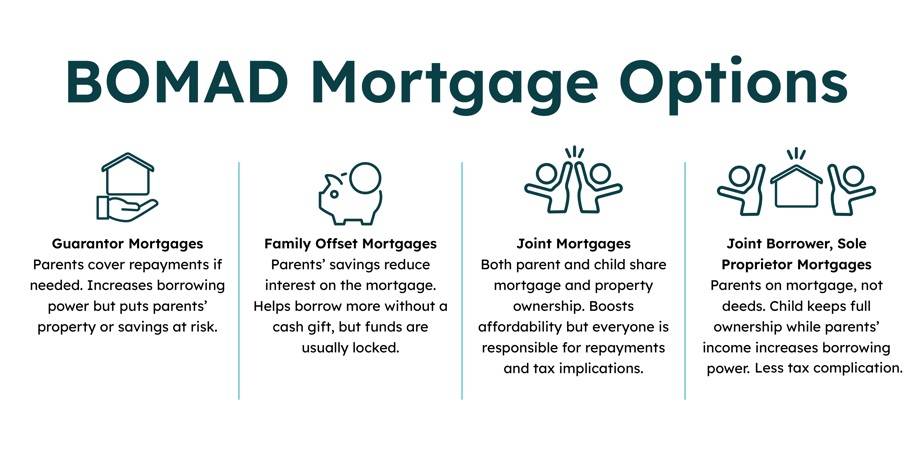

Bank of Mum and Dad mortgage options:

With a guarantor mortgage, parents agree to cover repayments if their child is unable to. This arrangement increases the child’s borrowing power because the lender views the loan as less risky. In many cases, the guarantee must be secured against the parents’ own home or savings.

While this support can be invaluable, the risk is significant: if the child defaults, parents could face repossession of their property or loss of their savings. Guarantor mortgages are less common in today’s market but are still available through specialist lenders.

A family offset mortgage allows parents to place their savings into a linked account that reduces the balance on which the child pays interest. For example, if a child takes out a £200,000 mortgage and parents deposit £40,000 into the offset account, interest is charged only on £160,000.

The parents keep ownership of their savings, but the money is usually locked away for a fixed period. This type of mortgage can help a child borrow more without requiring an outright cash gift. Availability is limited, with most products offered by building societies.

Some families choose a joint mortgage, where both parent and child are named on the mortgage and on the property deeds. This approach boosts affordability because the lender considers all applicants’ incomes.

However, it also means that everyone named is equally responsible for repayments, and any missed payments will impact all credit records. Parents who already own a property should be cautious, as being on the deeds of their child’s home can trigger the 3% additional stamp duty surcharge for second homes.

Joint ownership also brings complications around inheritance planning and may expose parents to Capital Gains Tax if the property is later sold at a profit.

An increasingly popular alternative is the joint borrower, sole proprietor mortgage. Here, parents are named on the mortgage but not on the property deeds. This allows their income to be included in affordability calculations without making them legal owners of the property.

As a result, the child remains the sole legal owner, which avoids the second-home stamp duty surcharge and simplifies inheritance matters. Parents are still financially liable for repayments, so lenders will conduct detailed affordability checks on them. This option offers a balance between boosting borrowing power and reducing tax complications.

Legal Considerations

It’s essential to get the legal details right. Whether it’s a gift, loan, or investment, formal agreements help avoid misunderstandings and protect everyone’s interests.

- Clarify the nature of the contribution: Is it a gift, a loan, or an investment? Each has different legal and financial implications.

- Use a Declaration of Gift: If parents are gifting money, this document confirms no repayment is expected, and is often required by mortgage lenders.

- Draft a Loan Agreement: If the money is a loan, outline repayment terms, interest (if any), and what happens if circumstances change.

- Consider a Declaration of Trust: If parents are contributing to the purchase price, this document defines ownership shares and what happens if the property is sold.

- Seek independent legal advice: All parties should understand their rights and obligations before signing any agreements.

- Factor in inheritance and tax implications: While cash gifts such as a house deposit are usually tax-free when given, they may count toward the giver’s estate for inheritance tax if they pass away within seven years (the current tax-free threshold is £325,000).

- Inform your mortgage lender: They need to know about any third-party contributions, which could affect the mortgage offer.

- Plan for future changes: Consider what happens if your child wants to sell, remortgage, or add a partner to the property title.

Considerations for Parents

Before gifting or loaning money to your children consider the following points:

- You may be using funds that you will later need for retirement or care.

- If you die within 7 years of giving a tax-free gift, your child will have to pay tax on it.

- If you take on a guarantor role then you will be responsible for the mortgage if your child cannot pay.

Considerations for Children

Asking your parents for money to fund a house purchase can cause tension so make sure it is something you can all afford.

- Be realistic about affordability: Make sure the arrangement doesn’t put financial strain on your parents, especially if they’re nearing retirement or have other commitments.

- Communicate openly: Honest conversations about expectations, repayment (if applicable), and future plans can prevent misunderstandings and keep the peace.

- Respect boundaries: Your parents may want input on the property or how it's managed. Set boundaries early on.

- Plan for independence: Consider how you’ll manage the mortgage, bills, and maintenance costs without ongoing parental support.

Buying through Shared Ownership

Shared Ownership can be a practical alternative to relying on the Bank of Mum and Dad, as it requires a smaller deposit than purchasing a property outright.

Under the scheme, buyers purchase a share of a home — typically between 25% and 75% — and pay rent on the remaining share, which is owned by a housing association.

Because the mortgage only covers the purchased share, the upfront deposit is based on that smaller amount, making it more accessible for first-time buyers with limited savings.

Over time, buyers can increase their ownership through Staircasing, purchasing additional shares until they eventually own the property outright. This route can help young buyers get onto the property ladder independently, without needing large financial contributions from family.

Case study: How parental advice led to Shared Ownership success

Maddie and Mason, first-time buyers with a young son, struggled to save a large deposit while renting. After living with Maddie’s mum for several years, they were unsure how they would ever afford a place of their own – until her mum suggested Shared Ownership.

With a £10,000 deposit (built from savings and family inheritance), they bought a 30% share of a two-bedroom home at Peabody’s Limebrook Walk development. Shared Ownership gave them the chance to secure a family home sooner, with lower upfront costs and the flexibility to buy more shares in the future.

Maddie says: “It was actually my Mum who suggested Shared Ownership as you can buy a property with a lower deposit — it’s made such a difference for us.”

Frequently asked questions about buying a home with the bank of mum and dad

Not immediately. Tax may only apply under inheritance tax rules if the parent passes away within seven years of the gift.

It depends on the agreement. That’s why it’s essential to put loan terms in writing to protect both sides.

It can be, but parents need to understand they are legally responsible if repayments are missed.